Why ProfG & Pomp/Visser are Wrong About AI

I was working out this morning with earbuds in, working through two podcasts back to back, when something started to make me curious. The first podcast was Anthony Pompliano’s conversation with macro investor Jordi Visser on The Pomp Podcast, published February 28, 2026, where the two picked apart the viral Citrini Research paper that had just rattled software stocks and drawn a response from the White House. The second was Scott Galloway’s Prof G Markets episode from March 2, 2026, covering much of the same ground. Both conversations were smart. Both were incomplete in ways that kept bothering me the longer I listened. And somewhere in the middle of my time on the treadmill, I started asking myself a question that neither podcast really touched. Why has the United States produced so much productivity growth over the past five decades, and why has almost none of it flowed down?

I have some skin in this game. I’ve been involved in many technology companies over the course of my career. I created jobs. I have done well. I genuinely believed for a long time that the rising tide was lifting boats, that the companies I was building were contributing to something broadly good. And now as I look at the actual data, I realize I needed to think harder about what I had been part of.

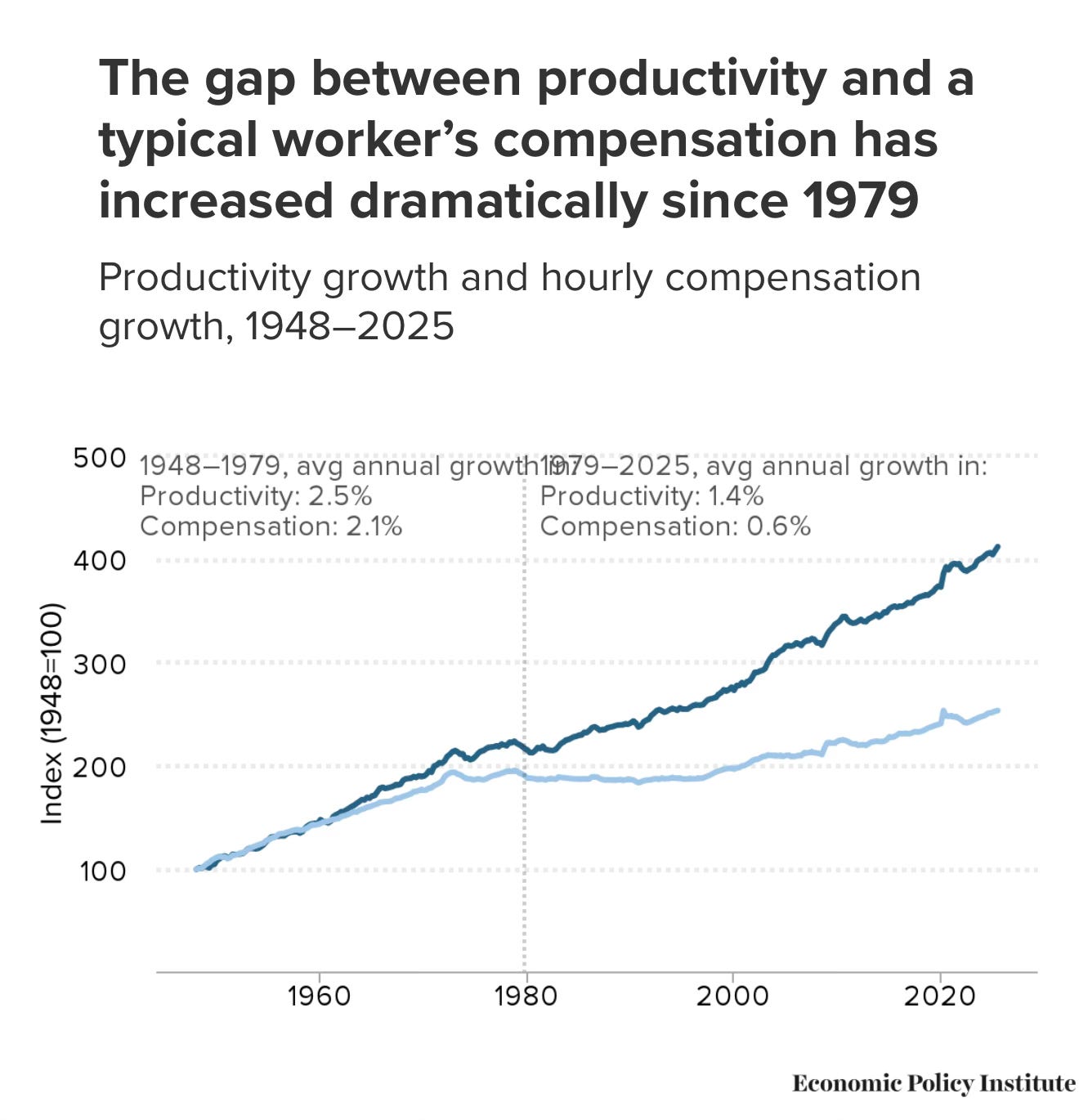

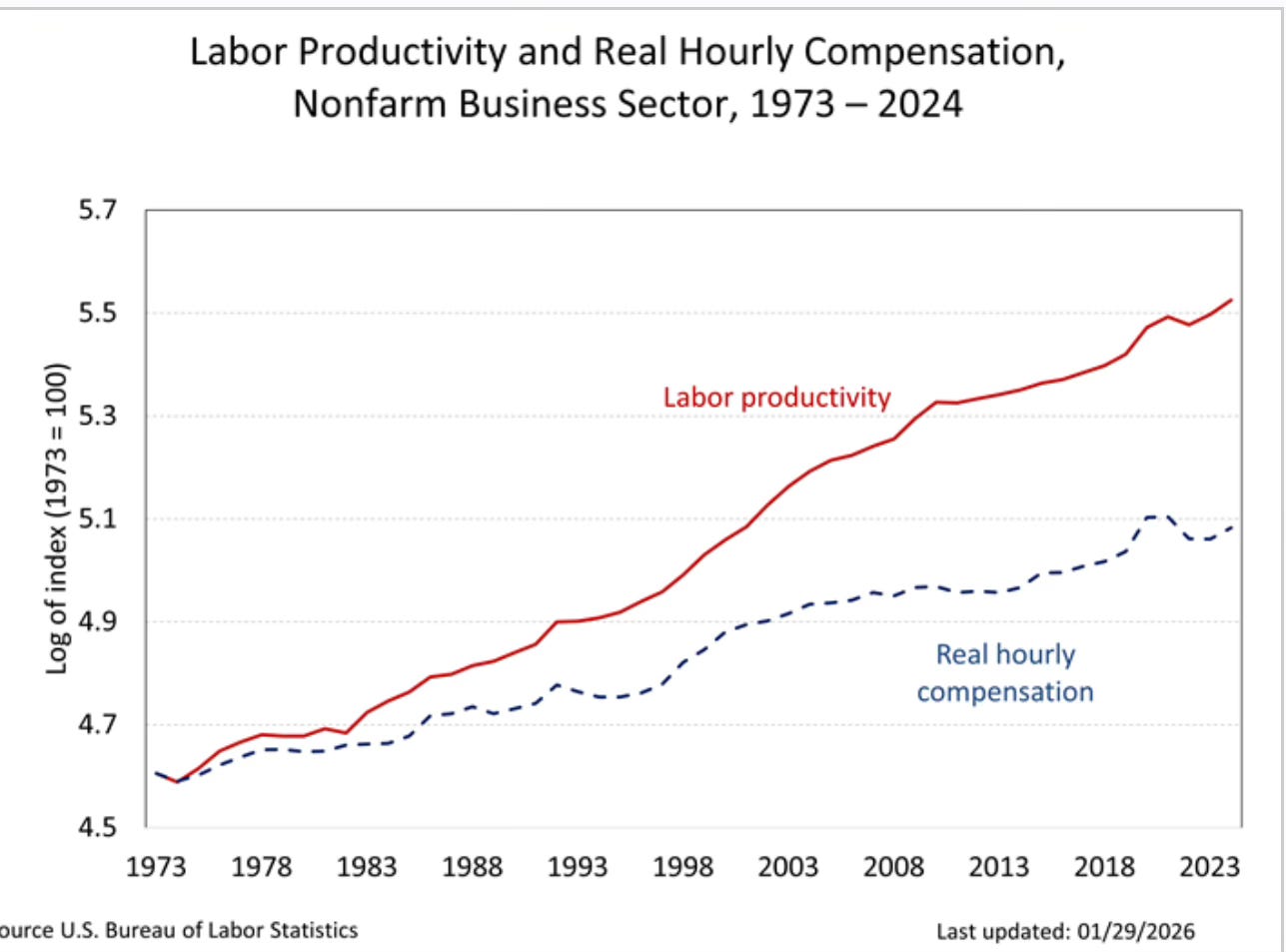

The numbers tell a story, though that story needs to be read carefully. From 1947 to 1973, productivity and real hourly compensation grew in near lockstep, each rising roughly 2.6 to 2.8 percent annually. The economy was generating surplus and that surplus was moving in both directions, up to capital and out to workers.

After that, something changed. Since 1979, Bureau of Labor Statistics data shows productivity rising approximately 90 percent through 2025, while real median hourly wages grew roughly 33 percent. That headline figure is real and important, but it requires a methodological footnote that I will not gloss over. The 57 percentage point gap partly reflects the use of different inflation measures for the two series: a consumer price index to deflate wages, and an output price deflator to measure productivity. Because these indices have diverged since the 1970s, with consumer prices rising faster than output prices, the gap looks larger than it would if measured consistently. When economists use the same deflator for both and include the full cost of employer-provided benefits in compensation, the raw gap shrinks.

But here is the critical point the methodology critics tend to miss. When EPI and others control for this by using a unified deflator, they find that 81 to 92 percent of the remaining divergence is explained by two things that are indisputably real: the rising share of total compensation going to the highest-paid workers, and the declining share of national income flowing to labor overall versus capital. BLS data confirms that labor’s share of nonfarm business output fell from roughly 65 percent of total output in the mid-1970s to approximately 57 to 58 percent by 2017, and the slide has continued. In other words, the exact size of the gap is debated. That a substantial and consequential gap exists, driven by rising inequality rather than statistical quirk, is not.

The story is not that workers were paid less than they produced in some absolute sense. The story is that a rising share of what they produced was captured by the people at the top of the income distribution rather than distributed broadly.

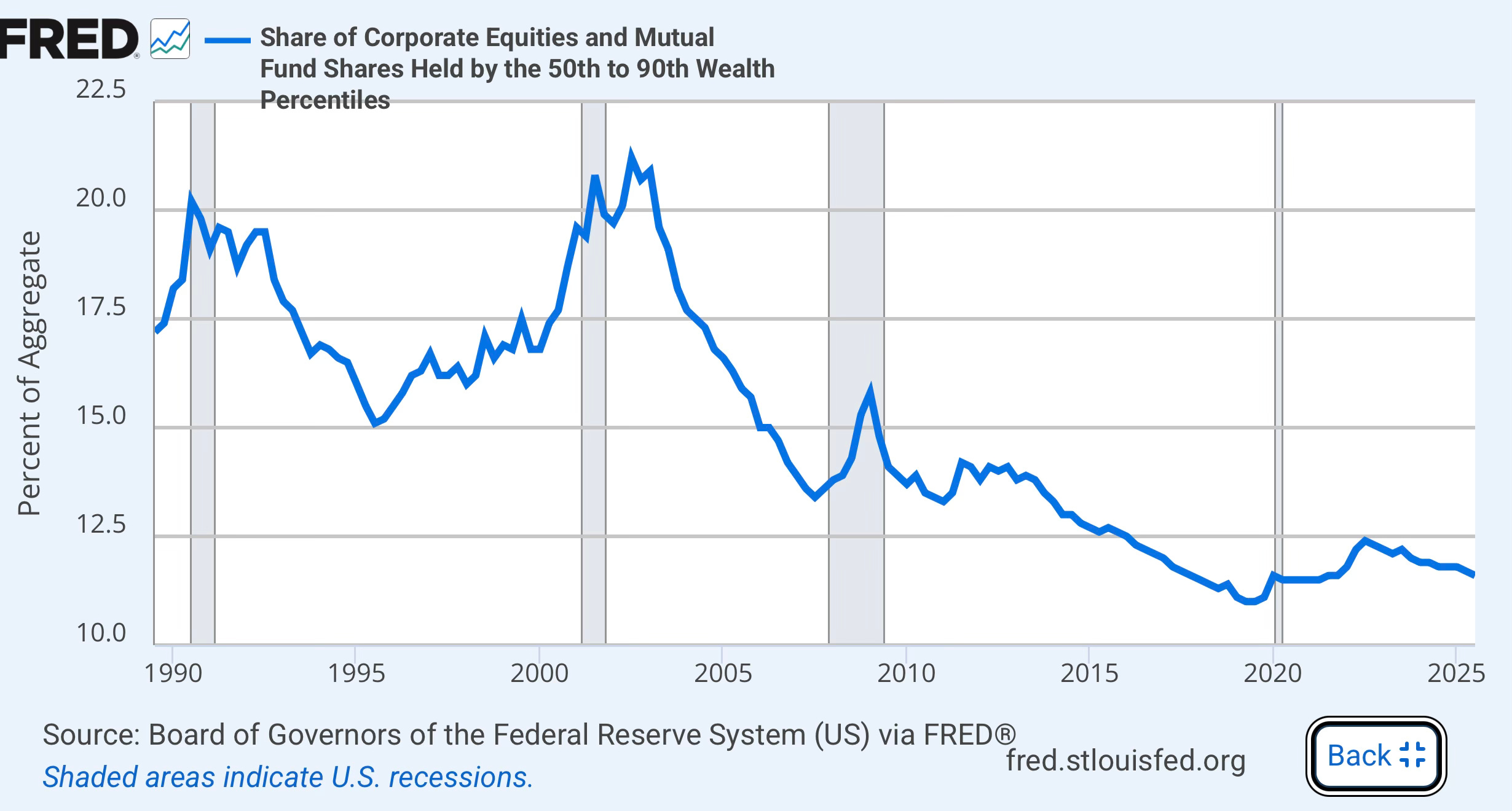

Where did the difference go? Federal Reserve distributional accounts show the top 10 percent of Americans owning approximately 87 to 93 percent of corporate equities and stocks.

When productivity gains flow to shareholders, they flow overwhelmingly to a thin slice of the population. A 2013 EPI analysis found that CEO pay at the 350 largest public U.S. firms had risen from roughly 20 times typical worker pay in 1965 to close to 300 times. That growth was not tied to greater individual productivity. It was tied to the restructuring of who inside corporations got to claim the surplus.

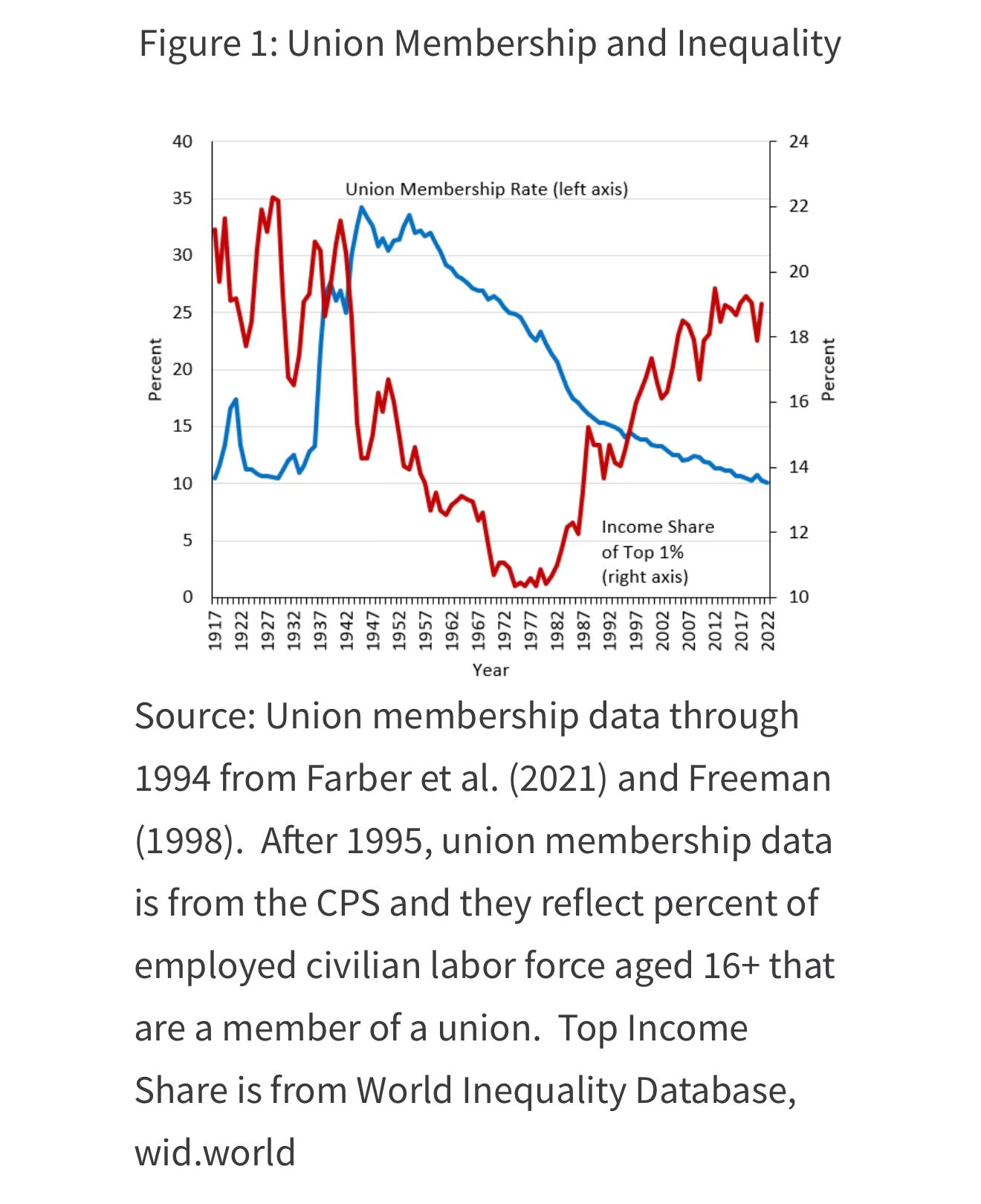

Private sector union membership peaked near 35 percent in the early 1950s, held above 30 percent through the 1960s, and has fallen below 6 percent today. When unions were strong, they established wage floors that even nonunion employers had to partially match to compete for workers. That competitive pressure is what historically transmitted productivity gains into broad wage growth. Remove it, and the transmission mechanism breaks.

Now I want to explain the mechanism, because understanding it as a system is what makes the AI question so consequential.

Technology tends to replace labor and augment capital. The people who own the machines, the software, and the platforms capture the gains. Because ownership of productive assets in the United States is extraordinarily concentrated, a productivity gain that flows to shareholders reaches very few households.

As industries consolidate, employers gain wage-setting power over workers. Economists call this monopsony. When Amazon is the dominant employer in a county, or when hospital systems have merged until there is effectively one option for nurses in a region, workers have nowhere else to go. Research using BLS and Census data consistently finds that rising labor market concentration suppresses wages even when productivity is rising.

Digital technology created natural monopolies at a scale previous eras never produced. The marginal cost of serving another user on Google or Meta is near zero. The returns on that near-zero marginal cost concentrate in equity held by founders and early investors. These platforms do not need large workforces to generate enormous value, so the value they create does not move through labor markets the way a steel mill’s productivity once did.

Capital gains are taxed at lower rates than ordinary income. Estate taxes have been progressively weakened. These are not laws of nature. They are choices, made by legislators who are largely funded by the people who benefit from them. Policy reinforces market outcomes rather than correcting them.

Finally, technology has consistently complemented high-skill cognitive work while substituting for routine work at middle and lower skill levels. This hollows out the middle of the wage distribution. High earners become more productive and more valuable. Routine workers get pushed into lower-wage service work. Labor economists call this polarization.

These forces interact and reinforce each other. They are not separate grievances. They are one algorithm. And in the United States, unlike Germany or Denmark, the institutional choices made over 50 years allowed that algorithm to run at full speed.

Germany maintained strong sectoral unions through its codetermination system, which legally requires worker representation on corporate boards. Denmark negotiated wage floors at the industry level. These nations had access to the same technologies. They produced significantly less extreme inequality outcomes because their institutional rules were different.

I should address Japan directly as it does show lower income inequality than the United States by Gini coefficient measures, and its CEO pay ratios remain far more compressed. But Japan also suffered roughly three decades of near-zero economic growth and persistent deflation after its asset bubble burst in 1991. Its real wages stagnated across the board, not because gains went to the top, but because growth itself collapsed. Japan offers a caution, not a model. Better distribution of a stagnant pie is not obviously better for workers than unequal distribution of a growing one. What Germany and Denmark offer is the more instructive contrast: they achieved both more equitable distribution and comparable economic dynamism, suggesting the U.S. outcome reflects institutional choices, not economic inevitability.

The technology creates the opportunity for concentration. The rules determine whether that concentration compounds unchecked. I know this from the inside. Building companies felt like creation and contribution, and it was. But I was operating within a set of rules I did not design and did not question, rules that systematically directed the surplus I helped create toward people who already had capital, including me, and away from many of the people whose labor made it possible.

Now, why did the economy keep working? This matters enormously for understanding where the breaking point is with AI.

The postwar alignment was the clearest version of a virtuous cycle. Productivity gains were broadly shared, which generated consumer demand, which justified further investment, which created more jobs and more productivity. That cycle ran for roughly three decades.

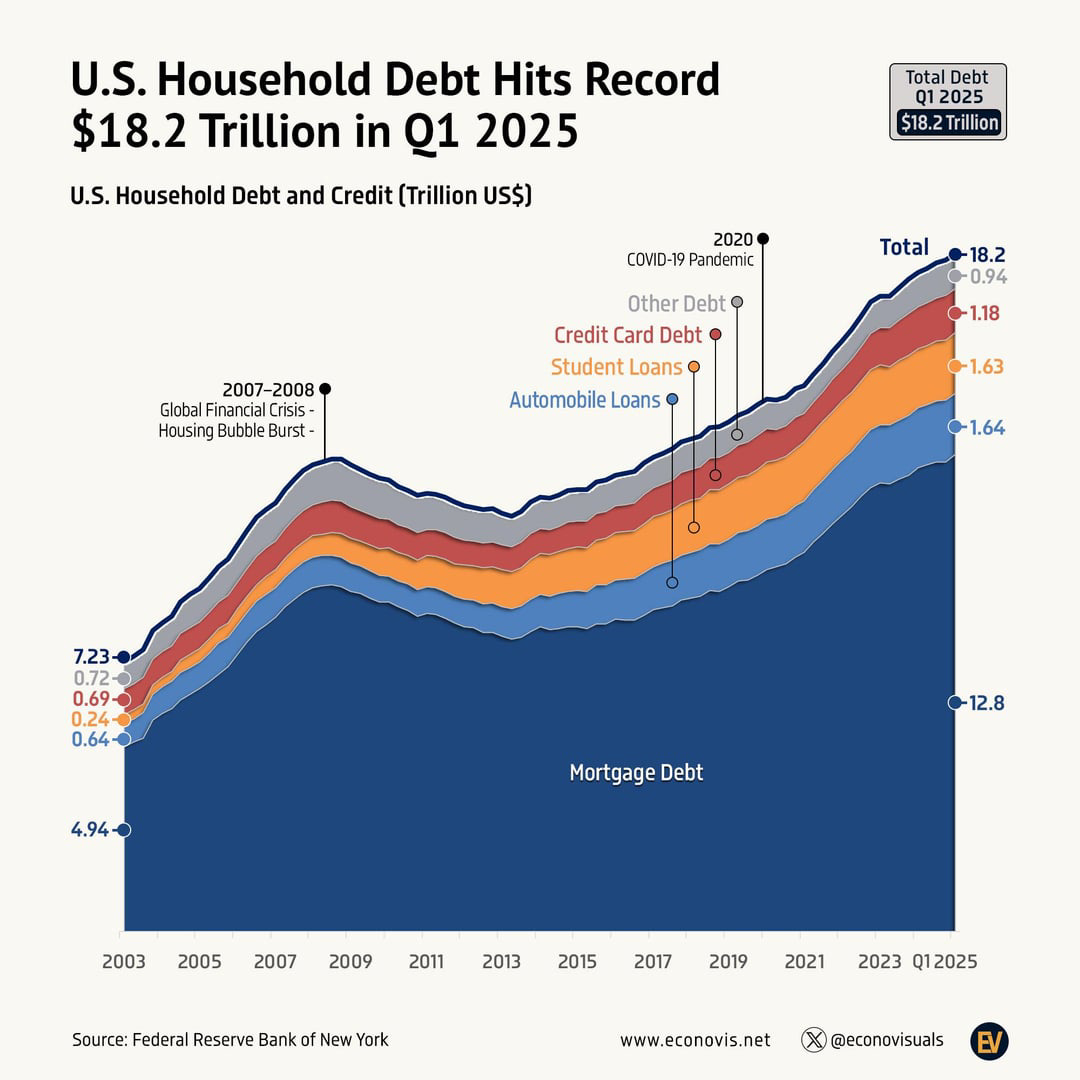

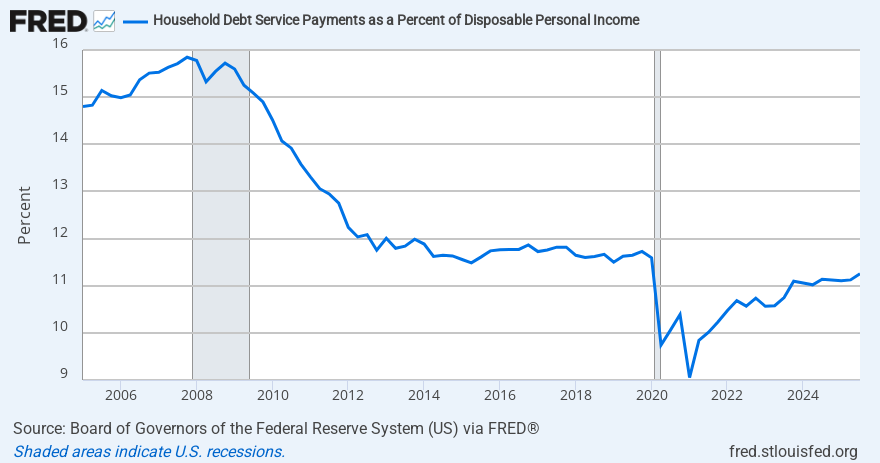

After the divergence began in the late 1970s, the economy kept growing through a different mechanism. American consumers, whose wages were stagnating relative to productivity, maintained their spending levels by borrowing. Household debt as a share of disposable income rose steadily from the 1980s through 2008. Credit cards, home equity loans, and eventually the mortgage products that triggered the financial crisis all served the function of keeping consumer demand alive even as labor’s share of income fell. The productivity gains went to capital. Capital recycled some of that back through lending. Consumers borrowed to sustain spending. The cycle continued.

This was a coherent, if fragile, system. The fragility became visible in 2008 when the debt load became unsustainable. The recovery from 2009 onward was slower and more unequal than any recovery since the Depression. The debt mechanism was partially exhausted and nothing replaced it as a broad driver of demand. The gains continued flowing upward. The economy kept growing, but the growth became increasingly concentrated in asset prices and the incomes of those who owned them.

This is the context that neither podcast addressed when discussing the Citrini paper.

James Van Geelen of Citrini Research, writing a hypothetical dispatch from June 2028, described a scenario where AI-driven productivity causes corporate profits to surge even as mass layoffs hollow out the consumer base. He called the result “ghost GDP,” output that shows up in the national accounts but never circulates through the real economy because, as he put it, machines spend zero dollars on discretionary goods. In the scenario, unemployment reaches 10.2 percent and the S&P 500 falls 38 percent from its October 2026 highs.

In macroeconomic accounting, every dollar of output equals a dollar of income somewhere. If a machine produces value with no human labor, that value does not vanish. It accrues as profit to the owner of the machine. The money does not become a ghost. It pools in the accounts of capital owners and corporations, and from there it moves into asset markets rather than consumer goods markets.

This is an important distinction. The problem Citrini identifies is not a breakdown in the accounting. It is a breakdown in what economists call the velocity of money. When gains pool at the top of the income distribution rather than circulating as wages across the broader population, the spending multiplier on those gains shrinks dramatically. Wealthy households have a much lower marginal propensity to consume than working-class and middle-class households, which spend nearly all of additional income. So the money exists, but it moves into stocks and real estate rather than into the grocery stores, car dealerships, restaurants, and service businesses where it would otherwise sustain demand and employment.

This is the real mechanism underneath the ghost GDP concept, and it is already visible in the data we have, not just in a hypothetical 2028 scenario.

On the Pomp Podcast, Pompliano and Visser pushed back on the Citrini framework, arguing that the timeline was too compressed and the scenario too deterministic. Visser, with over 30 years of macro investing experience, made the case that markets were overreacting and that AI’s productivity gains would ultimately find their way through the economy in value-creating ways. He also argued, compellingly, that the fiat financial system’s guardrails cannot handle the speed of AI agents operating autonomously. That is a real infrastructure problem worth taking seriously, and it is distinct from the distribution question I am raising here.

On Prof G Markets, Galloway called the ghost GDP concept “arguably fair only up to a point” before suggesting the scenario tips into unrealistic doomerism.

Both shows have a point about the specific Citrini projections. Extrapolating to 10.2 percent unemployment within a two-year window requires a set of assumptions that deserve scrutiny. But here is what both shows missed.

Ghost GDP is not a future scenario. It is a description, with a more precise name, of what has been happening for 45 years. And there is something else neither podcast mentioned: the evidence already showing up in the labor market for educated workers.

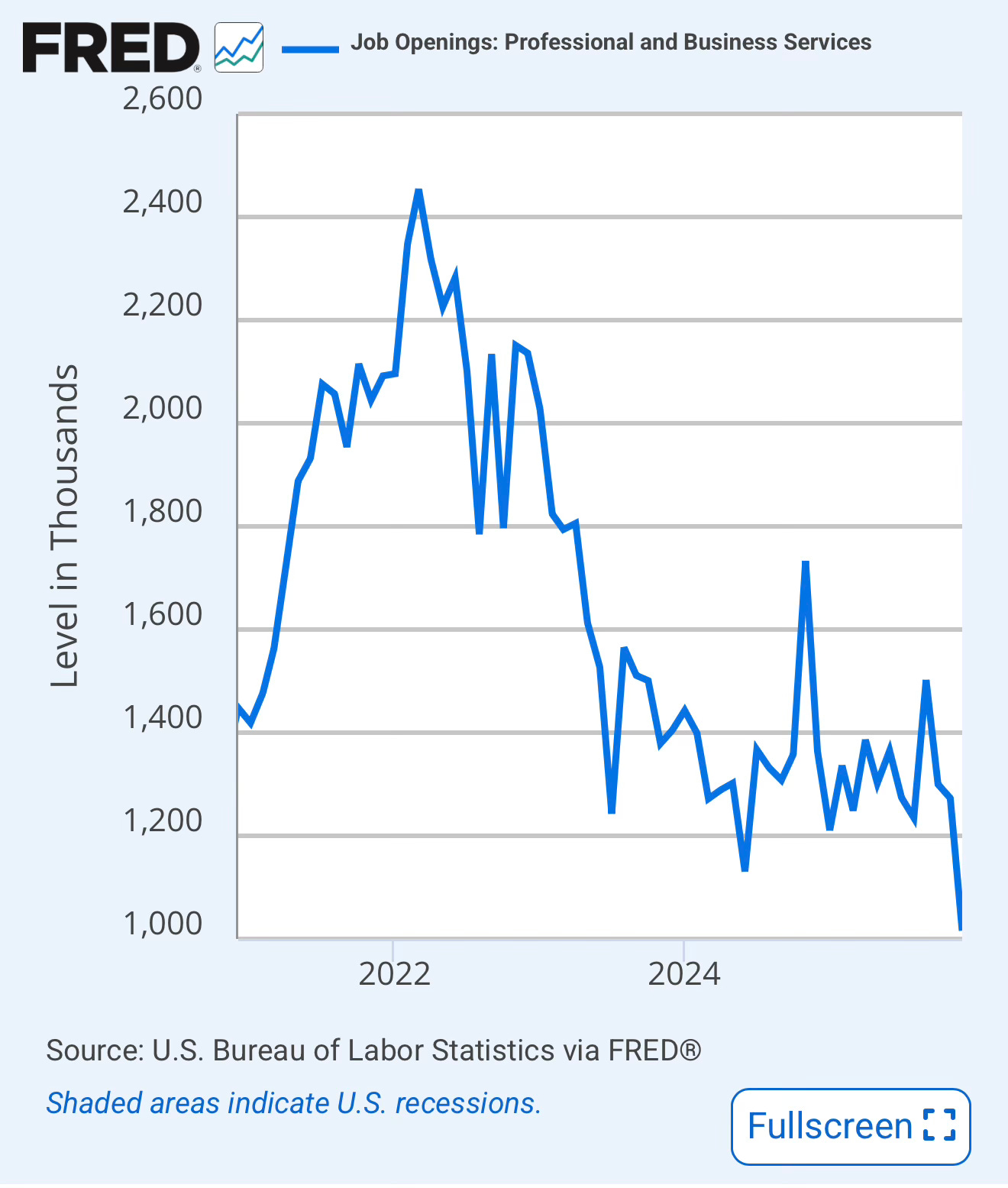

The white collar job market has been contracting in ways that are measurable and documented. In January 2025, the BLS reported the lowest rate of job openings in professional services since 2013, a 20 percent year-over-year drop. Job openings in the information sector alone fell by 73,000 between December 2023 and December 2024. The professional unemployment rate rose to 4.2 percent from 3.1 percent a year earlier. Computer science graduates faced 6.1 percent unemployment in 2025, roughly double the rate of philosophy majors, completely inverting the career advice that had been given to students for a generation. The hiring rate for positions paying over $96,000 dropped to a decade low.

The 2023 through 2025 white collar contraction was substantially driven by macroeconomic forces, not primarily by AI. The end of the zero interest rate policy era, aggressive Federal Reserve rate hikes, and a massive pandemic-era over-hiring spree in technology and finance created a structural correction. Companies that had grown their headcount irrationally during an era of free money were forced to right-size. You can’t attribute the current contraction all to AI as that would be conflating a cyclical shock with a secular shift.

But what the 2025 data shows, looking specifically at year-end Challenger, Gray & Christmas data, is that AI-attributed job cuts are rising on top of the macroeconomic correction, not instead of it. In 2025, over 50,000 job cuts were explicitly cited as AI-driven, and the pattern shifted from broad pandemic-correction layoffs toward what researchers began calling “the Great Agentic Displacement,” a more surgical removal of entry-level white-collar roles as companies transitioned from AI as a tool to AI as an autonomous agent. Federal Reserve Chair Jerome Powell said explicitly in October 2025 that “a significant number of companies” had cited AI when announcing layoffs or hiring pauses, adding that many employers were signaling they would not need to add headcount for years. “Job creation is very low,” Powell said, “and the job-finding rate for people who are unemployed is very low.”

The important question is not whether the 2023 through 2025 contraction was caused by interest rates or by AI. Both were operating simultaneously. The important question is what happens when AI productivity accelerates into a labor market that never fully recovered its entry-level rungs, and where the macroeconomic buffers are thinner than they were before 2008.

What AI is eliminating first is not the lowest-skill work. It is eliminating the entry-level rungs of high-skill career ladders, the positions that workers were advised to retrain into after previous waves of automation displaced them. When those rungs disappear, the pipeline of experienced senior professionals eventually dries up, but that consequence arrives with a lag long enough to make it easy to ignore in the near term.

AI is not simply another automation wave. Every prior wave displaced routine physical or cognitive tasks while leaving complex judgment, creativity, and communication to humans. The advice was always to move up the skill ladder. That advice was valid for several decades. Now AI is moving into legal research, financial analysis, software development, medical diagnosis, and content creation at accelerating speed. Anthropic CEO Dario Amodei has predicted that AI could eliminate half of all entry-level white-collar jobs within five years. The ladder that workers were told to climb is being sawed off from the bottom up.

Now let me be precise about where the virtuous cycle breaks, because this is where I think the conversation needs to go.

The U.S. economy runs on a loop. Productivity gains generate corporate profits. Profits generate investment. Investment generates employment. Employment generates income. Income generates consumer spending. Consumer spending justifies further investment. The loop sustains itself when enough of the productivity gain circulates back as broad consumer purchasing power.

The critical variable is not the total size of the productivity gain. It is the fraction of that gain that reaches households with high marginal propensity to consume, meaning households that spend most of their income rather than save and invest it.

The arithmetic is stark. If a productivity gain of one trillion dollars flows entirely to the top 10 percent, and those households consume perhaps 30 percent of marginal income, the demand stimulus is roughly 300 billion dollars. If the same trillion flows as wages across the income distribution, and median and below-median households consume 90 percent or more of marginal income, the demand stimulus approaches 900 billion dollars. The gap is not trivial. It compounds over time. This is not a political argument. It is arithmetic about how economies sustain demand.

The line that separates a virtuous cycle from a vicious one is the point at which the consumer spending multiplier on productivity gains falls so low that aggregate demand weakens faster than new investment can compensate. The United States has been approaching this line for decades, held back by debt-fueled consumption, federal deficit spending, and asset price inflation that made wealthy households feel prosperous enough to sustain spending at levels that kept the economy moving. None of those buffers are unlimited.

AI represents a productivity gain that will likely dwarf anything the U.S. economy has experienced since electrification in the early 20th century. Multiple research projections estimate AI could add several trillion dollars annually to global output within a decade. If that gain flows through the existing algorithm, concentrating primarily in capital and high-skill cognitive work, the demand multiplier on those gains will be very low. The economy will produce more. Less of it will circulate as consumer income. The gap between output and purchasing power will widen faster than any previous technological wave produced.

The line gets crossed when the consumer demand contraction becomes self-reinforcing. Businesses reduce hiring as demand softens. Reduced hiring further weakens consumer demand. Credit markets tighten as default risk rises, including in the 13 trillion dollar residential mortgage market that becomes fragile when white-collar borrowers with 780 FICO scores face structurally lower incomes. Asset prices fall, reducing the wealth effect that has been propping up high-income consumption. The loop that was virtuous becomes vicious. This is not speculation. It is the same mechanism that produced 2008, driven by a different trigger.

Goldman Sachs estimated in early 2026 that AI displacement could add approximately 0.3 percentage points to the unemployment rate in 2026 as a conservative baseline. That is a modest number. But it sits on top of a labor market that already has thinner buffers than it did before, a household debt structure that limits the capacity for further debt-financed consumption to substitute for stagnant wages, and a tax and policy environment that will, absent active intervention, channel AI’s productivity gains primarily to capital owners.

This is what I find most troubling about the current moment. It is not that AI will definitely produce the Citrini scenario. It is that we are running the same algorithm that produced 45 years of documented upward concentration, at a dramatically higher speed, with a much larger productivity gain to distribute, while our institutions are set up precisely as they were when this algorithm produced the outcomes in the data above.

Ed Elson said something on Prof G Markets that I think is the most important observation either podcast made, and I agree with it without reservation. He noted that investors are currently obsessed with what could go wrong, which is an unproductive basis for portfolio positioning, but that the government seems obsessed with what could go right, which is catastrophic for policy. The government’s current posture is essentially hands off, with active measures being taken to prevent other regulatory bodies from imposing guardrails on AI development. The stated theory is that unconstrained AI development will maximize American competitiveness and that benefits will distribute themselves through market mechanisms.

The 45 years of data I have described above should make clear why that theory is wrong. Market mechanisms in the United States have not distributed productivity gains broadly since the late 1970s. The algorithm is not self-correcting. The postwar sharing of productivity gains did not happen by accident. It happened because of strong unions, progressive taxation, robust antitrust enforcement, and corporate governance norms that included workers and communities as legitimate stakeholders. When those institutions weakened, the algorithm reverted to its default, which is concentration.

The policy instruments that would change the outcome are not radical. Substantially expanded income support would maintain consumer demand as labor market disruption accelerates. A worker reinvestment fund, financed by a levy on the productivity gains AI generates for its corporate beneficiaries, would help workers transition. Profit-sharing requirements that give employees a stake in the gains their companies capture would reconnect wages and productivity. Stronger antitrust enforcement to restore competition in labor markets would reactivate the competitive pressure that historically forced employers to share gains. None of these require dismantling markets. They require recognizing that markets, operating through the algorithm described above, produce a specific and well-documented outcome, and that outcome is not stable at AI scale.

Visser and Pompliano are right that AI will be transformative, that the Citrini projections deserve scrutiny, and that crypto infrastructure and blockchain-based verification will likely play important roles in the architecture of an AI-saturated economy. Visser’s point about the speed of fiat financial rails is a real technical problem worth solving. But the speed of financial rails is not the variable that determines whether AI’s productivity gains make most Americans better or worse off. The distribution of gains is the variable that determines that, and the distribution is driven by institutions, not by markets acting alone.

The people making the most optimistic case are, with few exceptions, people who own the capital that will capture the gains. I know this because I was one of them. The optimism is not dishonest. It is structurally conditioned. The people who benefit from the existing rules have both the incentive and the platform to explain why those rules are natural, fair, and optimal. The people who bear the costs have neither.

I built companies, created jobs, and came out well financially. I am writing this from Portugal, where my wife and I relocated in part because we can live well on what we accumulated. I am not confessing to villainy. But I am admitting that I operated inside an algorithm I did not fully understand, and that the collective operation of that algorithm by people like me, rational at the individual level, has produced a systemic outcome I am no longer comfortable treating as someone else’s problem.

AI is the biggest productivity wave in a century. Whether it also becomes the wave that finally crosses the line from virtuous to vicious cycle is not predetermined. It is a policy choice. The current U.S. policy, which is effectively no policy, is itself a choice. It is a choice to run the algorithm at maximum speed with no governor on the engine. The data says we know what happens when we do that.

It is unfortunately my belief that the people in a position to change the rules are too busy counting the gains to notice what is accumulating beneath them.