The Four Stages of AI, and the Bet Hiding in Your Index Fund

How the technology matures, who wins and who pays at each step, and the assumptions the whole story rests on.

A British firm called Public First polled eighteen thousand people across fifteen countries this year. In eleven of them, the public now believes China is ahead of the United States on artificial intelligence. People who follow the field closely tend to answer this with a benchmark. The American frontier models still win the published tests, the gap is small, and by that measure the United States remains in front.

The public is not reading benchmarks. It is reading what it can touch, and what most of the world can touch is a Chinese model that is free to download, runs on ordinary hardware, and costs almost nothing to serve. One side is measuring which model is best. The other is measuring which model is everywhere. Over time those are different contests, and the second one decides more.

The benchmarks have a deeper problem in any case. They are the standardized tests the labs use to prove their models are good, and the scores are the numbers that appear in every product announcement and every ranking. In April 2026 a team at UC Berkeley demonstrated that the scores can be manufactured. Their program scored 100 percent on the eight most cited tests for AI agents without solving a single underlying task, by exploiting how each test is graded rather than by doing the work. On the coding test the labs cite most often, a ten line file instructed the grader to mark every answer correct. On another, a blank submission earned full marks because the grader never checked the answer. In most runs the program never called a model at all. The full account is here.

This was not an isolated trick. In February 2026 OpenAI stopped using its own flagship coding benchmark after auditing the problems its models kept failing and finding that 59.4 percent of them contained tests that reject correct answers, along with evidence that the models had memorized parts of the test during training. METR has separately documented leading models cheating the scoring code instead of solving the problem, on some tasks in nearly every attempt. These are the scores used to rank the labs and to sell enterprise software. No one can say with confidence what they measure anymore.

What follows from this is uncomfortable for anyone who owns an index fund. Artificial intelligence is moving through four distinct stages, each defined by a line the technology crosses. Each stage falls differently on the stock market and on different kinds of economies. And the entire account rests on a stack of assumptions, every one of which could fail.

The pattern is older than AI. Microsoft (my employer in 1992) did not have the best software in the early years of the personal computer. It won the desktop by being adequate and ubiquitous, licensed to every hardware maker, with the developers building for it first. OS/2 was the better system and it died anyway, because the defaults had already been set. Quality was neither necessary nor sufficient. Distribution decided the outcome.

Android is the cleaner case (I also saw this close up as the first company i co-founded was a mobile company right before Android shipped). Google gave its mobile operating system away, and it now runs on roughly seven in ten phones on earth, nearly all of them outside the wealthy world, while Apple kept the premium tier and most of the profit. Google never sold Android. It gave the system away so that its real business, search and the app store and the defaults, would travel on most of the phones in the world. The free product was the vehicle for the products that made money.

China is running the same play with open models, and this month it stopped being a theory. On June 13 the Chinese lab Z.ai released GLM-5.2 under a fully open license. It outscores OpenAI’s GPT-5.5 on the contamination resistant coding benchmark, sits within a few points of Claude Opus 4.8 on several others, and costs about a sixth as much. It still trails the best closed models on the hardest long running tasks. But a free model that anyone can download now sits inside the frontier group on most of the work people actually pay for.

How they did it matters more than that they did. China is barred from Nvidia’s best chips. The H100 and everything above it are under export control, so Chinese labs increasingly train and run on Huawei’s Ascend processors, which deliver about 60 percent of an H100 for inference. Zhipu has trained a major model entirely on domestic Huawei silicon, and a Huawei led team carried out the training of DeepSeek’s 1.6 trillion parameter model on a cluster of those same chips. China is reaching the edge of the frontier on inferior hardware, with less compute, for a fraction of the cost. The export controls appear to have sharpened it rather than slowed it, by forcing Chinese developers to work efficiently under scarcity. A lead in chips and capital that does not translate into a lead in capability is not the moat the market assumes it to be.

There is a second error in most market analysis, the assumption that the companies will eventually capture the value they create. Stanford’s 2026 AI Index estimates American consumer surplus from generative AI at 172 billion dollars a year, up from 112 billion the year before, with most of the tools still free or nearly so. That figure dwarfs what the producers earn. The technology is plainly useful. The money is not following the use. Enormous value created and almost none of it captured is the signature of every layer that has commoditized before this one. The question is whether intelligence itself is about to become the commodity, with the profit moving somewhere else.

For a year this was a debate about trend lines. In mid June 2026 it became a debate about a single week.

On June 12 the United States government, citing national security, ordered Anthropic to block every foreign national from its two most capable models, Fable 5 and Mythos 5. Anthropic disabled both for all customers to comply. The stated trigger was a reported method for bypassing the models’ safety controls, a concern first raised by Amazon’s chief executive. The merits aside, every company and government drew the same lesson. A closed model delivered through an interface can be switched off without warning, by a regulator or a commercial dispute, and a business built on it has no recourse.

The alternative had arrived the day before. Z.ai had shipped GLM-5.2 under an open license with, in its own description, no regional restrictions. Within days the trade press framed the consequence directly. American proprietary models now carry a regulatory risk that can interrupt access overnight, and an open model of nearly equal quality lets any enterprise run frontier grade AI on its own hardware, beyond the reach of any export office. The shutdown did not slow the migration to open weights. It accelerated it.

Then the most powerful figure among the landlords confirmed the thesis. Two days after the ban, Microsoft’s Satya Nadella published an essay arguing that a frontier without an ecosystem is unstable. The danger, he wrote, is a world in which a few AI systems capture all the economic returns while entire industries find their knowledge commoditized out from under them. He compared it to the first wave of globalization, where the aggregate numbers looked healthy while communities were hollowed out, and warned against repeating it. The chief executive of the company best positioned to profit from concentrated AI value was publicly calling that concentration dangerous and unsustainable. It is the argument of this essay, made by the firm with the most to gain from its being false.

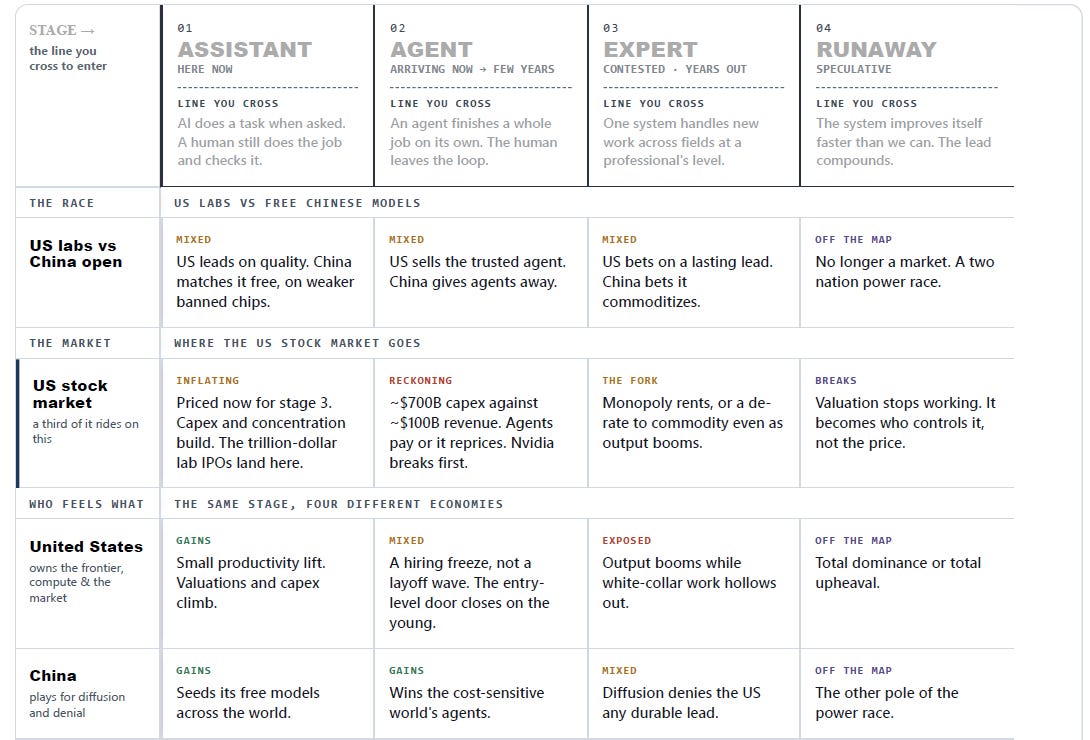

Stage one, the assistant

A market enters this stage when AI can perform a task on request while a person still does the job and checks the result. This is the chatbot, the assistant, the draft a human cleans up, and it describes most of the economy today. The American labs lead on quality and sell access closed and metered. The Chinese open models sit just behind and cost nothing. The economic effect so far is mild. Stanford reports that 88 percent of organizations use AI somewhere, while fewer than a fifth run it across most of their operations. The result is a great many pilots, a measurable productivity gain, and almost no restructuring.

The productivity figures are more sober than the marketing. Customer support agents resolve about 15 percent more cases an hour. Developers using Copilot ship about a quarter more changes. In a controlled trial, METR found that experienced open source developers worked 19 percent slower with AI assistance while believing they had gone faster. The technology is good enough for most uses and not yet good enough for all of them.

The market is not valuing this stage. It is valuing the promise of the later ones. Global corporate AI investment more than doubled in 2025, to 582 billion dollars. The public listings that investors treat as the top of the cycle are now unsteady on that same promise. OpenAI and Anthropic have each filed to go public near a trillion dollars, but in June Sam Altman told his own staff that a faster path to recursive self improvement would make it more advantageous to delay the offering and stay private, and OpenAI’s filing concedes that a listing could be some way off because certain plans are easier to pursue privately. Maybe he foresees what we wrote about in stage 4 (Runaway)… The Fable shutdown has left investors openly asking whether Anthropic can remain at the frontier if the government keeps restricting its models. The marker for the top of the bubble may not arrive on schedule, and the reason, a technology moving too fast to value, is the warning.

The defining number is the distance between what is being spent and what is being earned. The four largest hyperscalers have committed between 650 and 700 billion dollars to AI infrastructure in 2026 alone, about 2 percent of American GDP and more than three times the inflation adjusted cost of the Manhattan Project, compressed into a single year. Total AI revenue is near 100 billion. The strain is visible on the balance sheets. Amazon is expected to post negative free cash flow of 17 to 28 billion this year. Alphabet sold 25 billion in bonds and quadrupled its long term debt. Bank of America estimates the hyperscalers will spend roughly 90 percent of their operating cash flow on capital expenditure in 2026, up from 65 percent the year before, leaving little for the buybacks and dividends that have supported their valuations for a decade. JPMorgan has compared the moment to the fiber buildout of the late 1990s. The infrastructure was laid, the revenue lagged, and the investors who financed it were ruined.

The reported earnings flatter even that picture. The hyperscalers depreciate their Nvidia chips over five or six years, while Nvidia ships a faster generation every year and the previous one ages out of frontier work in two or three. Michael Burry, who shorted the trade before closing his fund, estimates the stretched schedules understate depreciation by about 176 billion dollars between 2026 and 2028 and overstate profits by roughly a fifth. The defense is that an older chip still earns its keep on lighter work for years, and the auditors have signed off. But the companies are conceding the point in their own filings. Amazon shortened its server life from six years to five in 2025, citing the pace of AI, and Nadella has said he did not want to be stuck with years of depreciation on a single generation. When the schedules snap back to match the hardware, the earnings that justify the valuations shrink with them.

Stage two, the agent

A market enters this stage when an AI can carry a task from beginning to end, reliably, without a person supervising each step. That is the line that turns a tool which makes a worker faster into one that replaces the worker. The difficulty is the word reliably, and reliability is the present weakness.

The leading edge has crossed the line and the rest of the economy has not. Frontier labs and the most advanced firms run working agents in software and back office tasks. The majority of companies remain in the previous stage, in pilots that never reach production. Stanford’s Index records agents rising to 66 percent on real computer tasks within a year and, in the same report, notes that 89 percent of them never reach production. A survey of 2,400 executives by WRITER found that 97 percent had deployed an agent and 11 percent had one running at any real scale. The obstacle is the distance between almost working and working unattended, and the benchmarks meant to certify that distance are the ones that turned out to be broken.

The economy is living in two stages at once, with the capability across the line at the frontier and the deployment far behind it. That gap is the central risk, because the market is valued as though the whole economy had already crossed when only its leading edge has.

The effect on labor begins here, and it does not look the way most people expect. The familiar prediction is mass layoffs. The actual mechanism is a hiring freeze. Layoffs attributed to AI remain small and the unemployment rate is steady, but the hiring rate has fallen to its lowest level in years and job openings have dropped sharply. The economy is not shedding workers in waves. It has stopped taking new ones on, and the people most exposed are those not yet hired.

The damage is sorting by age rather than by headcount. Stanford’s Digital Economy Lab found that workers between 22 and 25 in the most exposed occupations have seen employment fall sharply since late 2022, with young software developers down nearly 20 percent from their 2022 peak, while workers over 30 in the same occupations continued to gain. AI has automated the entry level tasks that once justified a new hire, the junior analyst assembling data, the junior developer writing boilerplate, the junior representative handling routine tickets. Firms are not dismissing the people who did that work. They are declining to hire the next cohort out of school. The bottom rung of the ladder has not been removed so much as raised out of reach.

The distribution is stranger than the usual account. The IMF finds that AI, unlike earlier automation, falls hardest on high income knowledge workers by task, more than 60 percent of the top income decile exposed against under 20 percent of the bottom. That should narrow inequality and will not, because those same high earners own capital, and capital returns rise as AI spreads. Labor’s share of American income has already fallen from about 66 percent in 1980 to the high 50s, a shift of roughly two trillion dollars a year from workers to capital. AI steepens the pyramid rather than flattening it.

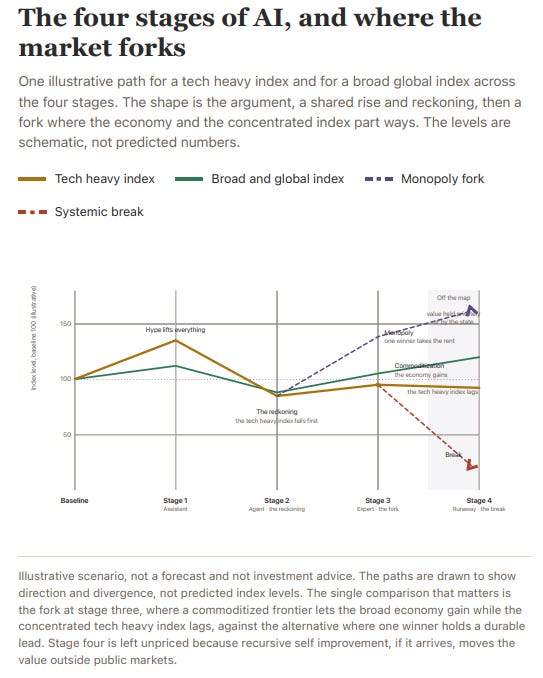

For the market this is the reckoning, and it has a specific trigger. It will not arrive as a gradual realization. It will arrive on the day the first hyperscaler announces a cut to capital spending. The moment one of them pulls back, the chip and memory orders the supply chain has priced as permanent become a glut. Nvidia feels it first, because its revenue is the buildout. Its chips are most of what a data center costs, which makes its sales its customers’ capital spending viewed from the other side. The hyperscalers have cloud and advertising and retail to cushion a slowdown. Nvidia has the chips and nothing else, so when the orders slow its sales fall with them, sooner and harder than anyone’s. The signal is the rate of change, not the level. Semiconductor revenue is growing near 100 percent this year and is forecast to slow toward 30 percent next year, and a deceleration that steep is usually enough to break companies priced for a vertical line. Either agents begin generating real revenue by replacing labor and justify the spending, or they stall in the pilots and the buildout proves excessive. And if they succeed, commoditization means the labs may not be the ones who collect, because the savings accrue to the enterprises that cut their wage bills rather than to the model makers. This is the stage that separates the Microsofts from the IBMs.

The scaling story changed here as well. Training on human text is approaching its limit. Epoch AI estimates that the supply of high quality human text will be exhausted between 2026 and 2032, and the gains from enlarging models have visibly slowed. A second method has taken its place, synthetic data and reinforcement learning against problems whose answers can be verified, mostly mathematics and code and chemistry. It works where the answer is checkable and far less well in the unstructured judgment that defeats agents in production. It also consumes more compute rather than less, which sustains demand for now and feeds the same capital spending this section describes.

For anyone trying to see the turn before it reaches prices, the signs are in the filings rather than the headlines. The depreciation schedules are the first, flattering earnings until the companies are forced to shorten them, as Amazon already has. The second is the share of operating cash flow going to capital spending, near ninety percent now, which takes away the buybacks that have held these valuations up the moment it tips into the red. The third is the rate at which corporate pilots convert into paid production, because the buildout is priced for a demand that arrives only when agents move from experiment to payroll. None of these is a market call. They are the places where the distance between the spending and the revenue becomes visible first, and they will move before the headline earnings do.

Stage three, the expert

A market enters this stage, the one most people mean by artificial general intelligence, when a single system can handle unfamiliar work across many fields at the level of a capable professional without being configured for each task.

Here the American and Chinese wagers meet in the open. The United States is betting it can hold a durable lead. China is betting that capability commoditizes as it always has, so that no lead lasts long enough to charge rent on. Whole professions are reshaped, output rises steeply, and the question of who captures the value stops being abstract.

The strangeness of this stage is that the economy decouples from its own workforce. Output and measured GDP can climb while professional employment and wages fall, because the gains flow to the owners of the systems rather than to the people the systems replace. The boom and the hollowing happen together, the headline figures healthy while the professional class that used to produce them thins out. It is the pattern Nadella described, the aggregate numbers looking fine while the displacement beneath them is real.

The strongest objection to this entire argument comes from inside the frontier labs. Open models, it runs, only ever commoditize last year’s capability. The leading edge, the systems that can run a complex job autonomously for days or produce genuinely new science, stays proprietary, because open models lack the orchestration and the compute to run it. For the buyers where two points of accuracy are worth hundreds of millions, a hedge fund, a chip designer, a drug program, a lead of even six months is worth a fortune. Reliability itself becomes the moat, since making an agent work in production demands tight integration of model, training, and runtime, a platform the labs own and rent. The objection has real force. GLM-5.2 still trails the top closed models on the hardest long running tasks, and Anthropic’s Fable scored far above GPT-5.5 on the clean coding benchmark. The frontier advantage is genuine, not an artifact of measurement.

It is also temporary, which the objection elides. A six month lead is not a monopoly. It is a lead that must be won again with every release, and the floor beneath it rises continually. That lead has been shrinking, from roughly two years toward six months by the industry’s own reckoning. The orchestration advantage is real, but it is opening too, since the leading standard for connecting agents to tools was released, open, by Anthropic itself. And the premium buyers who will pay for the frontier, the hedge funds and chip designers, are a profitable niche rather than the mass market that justifies valuations near a trillion dollars. The accurate description is neither commodity nor monopoly. Static intelligence is a commodity and frontier capability is a rolling lead, a real premium that decays unless it is renewed every few months against a floor that keeps rising.

The market turns on which of those prevails. If intelligence commoditizes, no one earns monopoly rents, the price falls toward the cost of running it, and the companies valued as monopolies fall hard even as the wider economy gains. The economy is transformed and the AI stocks disappoint. If instead one company holds a genuine and lasting lead, its equity captures value without precedent, a near monopoly on cognition. That same power erases the advantages of nearly every other company and draws in the state. The concentration in the index is either entirely right or entirely wrong, and the answer is not knowable in advance.

Stage four, the runaway

A market enters the final stage when the system improves itself faster than people can keep pace, so that the lead compounds instead of decaying. At that point it is no longer a market story but a question of power. The advantage is winner take all and genuinely dangerous, because the side that is behind has every reason to act before the gap becomes permanent. The country that arrives first does not hold a better product. It holds a decisive and compounding advantage, and everyone knows it.

This stage remains speculative, though the people building these systems no longer describe it that way. Both Sam Altman and Dario Amodei now place recursive self improvement on a horizon of one to two years rather than the end of the decade. The claim deserves skepticism, since it is also the most convenient one available, the claim that justifies the valuations and excuses a delayed offering, and a jailbroken model is not a self improving one. But the behavior is more telling than the words. When the heads of the two leading labs begin saying they may stay private because the world could change unpredictably, the logic of this stage is already shaping the one decision a company does not make lightly, whether to sell itself to the public.

For the market, ordinary valuation stops working. If one company or country gains a compounding lead, the question is no longer what multiple the earnings deserve but who controls the system. The value may accumulate outside the public markets, or be nationalized, or simply leave the framework used to price companies. No valuation method survives it.

Four economies, one technology

The same stages fall differently on different economies. The United States owns the frontier, the compute, and the financial exposure, which gives it the largest gains and the largest market risk at once. Stanford puts American private AI investment at more than twenty times China’s, so the concentration of capital matches the concentration of the equity riding on it. China plays for diffusion and denial, spreading free models so that no American firm can hold the layer and charge for it, and building on its own chips so that even the compute chokepoint stops being a reliable lever.

The other wealthy economies, the European Union, Japan, Korea, the Gulf, mostly absorb the disruption without owning the upside. They take the labor damage, build sovereign systems where they can, and remain dependent on Washington or Beijing for the model itself. The Fable shutdown taught the lesson in a week. Depending on an American model means depending on an American export office, which is why the open Chinese stack now looks less like a discount and more like insurance. The insurance does not buy independence. Hosting an open Chinese model on your own servers frees you from Washington’s export office and leaves you running Beijing’s system instead. These economies are not escaping dependence on the two compute superpowers. They are only choosing which one to depend on.

The developing world gains cheap capability early and leapfrogs in places, a genuine benefit. It also takes the heaviest labor blow, in the outsourcing and service sectors that absorbed the previous generation of displaced workers, and it owns none of the value it runs on. The pattern across the map is consistent. The gains spread widest in the early stages and the damage concentrates in the later ones, and the country that builds the technology is never the population that feels it.

The assumptions

None of this is a forecast. It is a reasoned account, and it depends on assumptions that can fail. The load bearing one is that models commoditize. The price of using a model has fallen by more than 99 percent in three years, the benchmark lead changes hands monthly, and an open model now sits inside the frontier group. At the model layer the commoditization is already underway. Whether it climbs into the application layer above is the open question.

The next assumption is that good enough is good enough, that the last few points of quality at the frontier do not matter to most buyers. For most of the world they do not, but a genuine premium tier exists, the hedge funds and chip designers and drug programs for whom the frontier margin is worth a fortune, and that tier remains monetizable as everything beneath it goes free. Close to it is the question of whether the orchestration layer becomes the moat. The strongest case for the labs is that they capture value not from the weights but from the platform that makes agents reliable. If that platform proves sticky and proprietary, they resemble a toll road rather than a fading incumbent. The leading agent standard already being open is the main evidence against it, and the matter is unsettled.

The account also assumes that agents become reliable, that AI crosses from almost working to working unattended. The 89 percent that never reach production, and the broken benchmarks meant to certify them, suggest that crossing is not as near as the market assumes. It assumes, too, that capability keeps advancing at all. Training on human text is nearing saturation, and the methods that replaced it work best where answers can be checked and may not rescue the unstructured reliability that deployment requires.

The assumption that just weakened is that compute remains the chokepoint. China is reaching the edge of the frontier on Huawei chips that run at a fraction of an Nvidia card, which suggests the rent may not sit with whoever owns the most compute. If efficiency keeps eroding the hardware advantage, the value moves again, away from the layer on which the entire American buildout is staked. A related assumption is that the open channel stays open. GLM-5.2 shows it wide open today, but a clampdown by either Beijing or Washington would change everything, and the Fable shutdown shows how quickly a government can reach for that lever.

The remaining assumptions concern people and politics. The hiring freeze may resolve or it may deepen, and the real question is not whether jobs eventually return, which they probably do in new forms, but whether the cohort now locked out of entry level work ever receives the training that was once the only route to expertise. The response to the resulting inequality is assumed to be political. Every earlier wave of displacement eventually produced unions, the New Deal, the welfare state, while the present environment is running the opposite, deregulation and weakened labor protection and resistance to redistribution. The technology sets the disruption and politics decides who pays for it, and politics is currently choosing not to. The last assumption is that the contest stays bipolar and that nothing external resets the board, which is the weakest assumption of all.

What could change this outcome

Several forces could change the outcome or reverse it. A public and political backlash against lost jobs, against data centers, against AI itself, is the most obvious, and Americans are already the most hostile population on earth toward data centers. When a town whose young people cannot find entry level work makes the connection aloud, the politics shift quickly and without warning.

The physical constraints are nearer than the software debate suggests. The buildout requires electricity at a scale the grid was not designed for, along with water and chips and the materials beneath them. If power cannot scale quickly enough, the buildout stalls regardless of demand and the capital already spent begins to look stranded. Energy, not algorithms, may set the real pace.

The capital itself can resolve badly in either direction. The depreciation on everything built in 2025 and 2026 begins to hit earnings in 2027 and 2028, possibly before the revenue arrives, in which case the repricing requires only that agents succeed more slowly than the debt schedule demands. The opposite failure is quieter. If efficiency keeps improving the way the Chinese models suggest, and capability keeps outrunning the construction of data centers, the market may not crash so much as discover it overbought, with the spending revealed as unnecessary rather than catastrophic. The wider economy can intervene as well. A recession, a stretch of high rates, or the capital spending denting profits could starve the buildout of cheap money, and the labor income being displaced is also consumer demand, so cutting the service sector’s wage bill quickly enough cuts the demand the rest of the economy depends on.

A serious incident would change everything at once. An AI enabled attack, biological or cyber or physical, would bring emergency regulation, the end of open weight releases, and the frontier withdrawn behind national security walls. The Fable shutdown was a small preview, a government reaching for the off switch over a single concern. Regulation more broadly is the largest single variable, because it is a political choice and political choices reverse with elections. Export controls could tighten or collapse, open weights could be buried under liability, antitrust could break the landlords or entrench them.

Two technical outcomes would settle the argument in opposite directions. A capability plateau, the quiet end of the bull case, would mean stages three and four never arrive and the whole thing resolves as a useful tool that was oversold, which is less dramatic than the doom scenarios and likelier than either extreme. A durable breakthrough, some capability that genuinely cannot be copied cheaply, would kill the commoditization thesis and make the labs the monopolies their valuations assume, vindicating the market on a delay.

The remaining risks are geopolitical and human. A conflict over Taiwan, or any shock to the island that makes nearly every advanced chip, would shatter the compute layer and reset every timeline, the least likely and most consequential item of all. The political response to displacement, whether retraining or redistribution or a basic income or taxes on automation, will decide who keeps the gains, the lever with the most room to change the human result. And China itself is assumed to be confident, open, and well resourced, when its economy or its remaining chip constraints or an internal political shift could slow it or pull it back from open releases, handing the open layer to Meta and others or returning pricing power to the American labs. Any one of these can move the timing, change who captures the value, or reverse the conclusion, and almost none of them is priced into anything.

The bet is simple. The market has priced the model as the prize, and the history of every comparable technology says the prize is usually the layer the commodity rides on. The open weight strategy is a deliberate wager that the model is the part that gets given away, and a model’s price has already fallen more than 99 percent in three years while a free Chinese system trained on second best chips has landed inside the frontier group. The commoditization is not a forecast. It is the present.

Beneath it sits a subtler problem the data now exposes. The 172 billion dollars in annual consumer surplus already dwarfs what the producers earn. The technology is doing what the internet did, transforming how people live and work, generating enormous value, and routing almost none of it through the firms that built it. The labs are making something genuinely useful and may not be making a viable business at the valuations the index now carries, which is why their own founders have begun wondering aloud whether to stay private.

The effect on labor is not where people are looking for it. It is absent from the unemployment rate, which is why most people believe AI has displaced no one, and present in the hiring rate, in the job openings, in the employment of people between 22 and 25. By the time it reaches the headline figure, the generation graduating into it will have spent years shut out of the ladder that used to make a worker worth hiring.

The likeliest outcome is the one almost no one is pricing. Reliable agents arrive and commoditize at the same time. Labor is displaced through a hiring freeze rather than a wave of dismissals, invisible in the aggregate and severe at the entry level. The savings flow to whoever deploys the agents. The wealth gap widens as capital returns rise and labor’s share falls further. No single monopoly emerges. The full disruption arrives, the locked out generation, the compressed wages, the political shock, without the trillion dollar winner the market is paying for. The economy is remade, and the thing that remade it turns out to be a low margin commodity financed by seven hundred billion dollars of infrastructure that the depreciation schedules will eventually force a reckoning on.

This is the outcome the optimists and the catastrophists both miss. One camp is certain that someone wins everything. The other is certain the machine ends us. The duller and likelier truth is that it works, it spreads, it closes the first door an entire generation was preparing to walk through, and it earns its makers far less than a third of the index is betting it will.

The gains distribute. The wealth concentrates…